Australia's Transport Fuel Problem — and How to Fix It

One of the world's great energy exporters cannot reliably fuel itself. The exposure, what it costs, and the path from import dependence to net exporter.

Added the fiscal costs the per-litre comparison never counted: the standing Fuel Tax Credit that also suppresses electrification (§10), and the 2026 crisis excise relief as forgone revenue, with the pricing sovereignty a producer holds and a price-taker lacks (§9). New text is marked in blue.

Australia is one of the world's great energy exporters, and it cannot reliably fuel itself. It imports about nine in every ten litres of refined fuel it burns, holds the thinnest emergency reserve in the developed world, and runs the whole arrangement on ships it does not own, through a chokepoint on the other side of the planet. In 2026 that arrangement was tested and it bent. This memo sets out — with the numbers — how exposed the country is, what the exposure costs even when nothing goes wrong, and the path that ends it: cut the demand we can, make the rest at home, and turn the surplus into exports — from importing finished fuel to manufacturing and selling it.

1. How exposed we are

Start with the danger, because it is the part most often left out.

The fuel in an Australian bowser does not come from an Australian well or an Australian refinery. The chain that ends at that pump begins in the Persian Gulf. Australia imports around 90 per cent of its refined fuel, and the great majority of it is refined in Singapore, South Korea and other Asian hubs that themselves run on Middle East crude — most of it moving through the Strait of Hormuz. A disruption at that chokepoint never has to touch an Australian ship to reach an Australian pump. It only has to touch the tankers feeding the refineries that supply us.

Behind that long chain sits the thinnest buffer in the developed world. Australia holds on the order of a month's cover of the fuels it depends on — well below the ninety days it is obliged to hold as a member of the International Energy Agency, a standard it is the only one of the agency's members never to have met, not once since 2012. The agency's members average well over a hundred days. Australia has tens.

In 2026 the test came. When Hormuz closed, diesel passed three dollars a litre in the cities and approached four in remote communities, service stations ran dry, and officials modelled rationing if diesel stocks fell toward ten days. The country was, in plain terms, about a month of insulation away from a foreign incident emptying its pumps — and it nearly found out exactly how far.

2. The paradox

And yet Australia is an energy superpower. It is one of the largest exporters of liquefied natural gas on earth, the largest exporter of iron ore, the second-largest exporter of coal. It has more sun and wind than almost any nation alive. And it produces oil — around 400,000 barrels of petroleum liquids a day, most of it light condensate drawn from its gas fields.

Almost none of that production fuels Australia. More than 94 per cent of the oil the country produces is exported — light, sweet crude and condensate shipped to refineries across Asia — while Australia imports about 90 per cent of the refined fuel it actually uses, and brings in the heavier crude its own two refineries are built to run on. The country pumps oil, sends it overseas to be refined, and buys its petrol and diesel back from the same region it sold the crude to.

Table 1 — The supply gap (barrels per day, approximate)

| Flow | Volume (b/d) | Note |

|---|---|---|

| Petroleum liquids produced | ~400,000 | mostly light condensate from gas fields |

| Of that, exported | >94% | light sweet crude/condensate to Asian refineries |

| Total liquid-fuel consumed | ~1,150,000 | Australia ranks ~20th in the world for oil use |

| Refined product imported | ~850,000 | ~70–90% of consumption depending on month |

| Domestic refinery output | ~230,000 | capacity; covers only ~20% of demand |

Sources: EIA Australia Country Analysis 2025; Worldometer/EIA 2024; Australian Petroleum Statistics; Geoscience Australia, Australia's Energy Commodity Resources 2025.

It exports the energy and imports the fuel. The nation that ships the world its coal and gas cannot keep its own trucks running through a crisis. That is not a resource problem. It is a supply problem — a decision, made and remade over years, to sell what we produce and buy back what we burn.

3. Demand is growing, not shrinking

Liquid fuel is not a side issue for Australia; it runs the economy. The government's own 2019 Liquid Fuel Security Review put it plainly:

Liquid fuel is the backbone of the Australian economy. Liquid fuel underpins every aspect of our daily life, from our groceries to our commute to work and our emergency services. On average, each Australian uses nearly three times more energy from liquid fuel than they do electricity. Australia spends $57 billion on liquid fuels each year — more than electricity, at $38 billion; and gas, at $37 billion.

— Liquid Fuel Security Review, interim report, April 2019

The whole case for relying on imports rested on a quiet assumption: that demand would level off and then fall as the country electrified, so the exposure would shrink on its own. It has done the opposite. Transport fuel use has kept climbing, and the fastest growth is in the fuel hardest to replace — diesel.

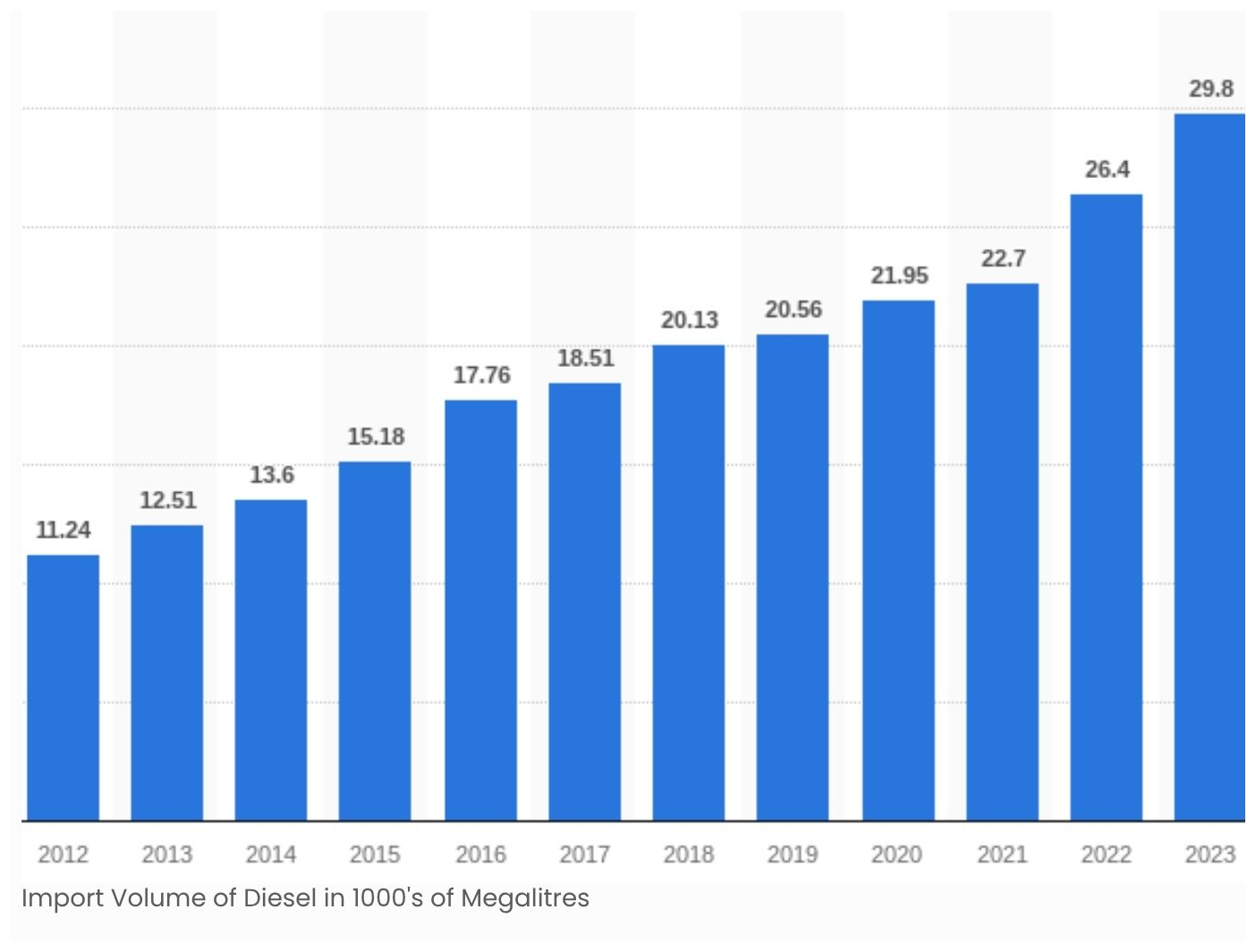

Australia's diesel imports rose from 11.24 thousand megalitres in 2012 to 29.8 thousand in 2023 — they nearly tripled in eleven years, and by 2025 about 91 per cent of the diesel the country burns is imported. Diesel is the fuel that moves freight, runs mining and agriculture, and backs up essential services; it is the hardest part of the task to electrify quickly, and it is the part growing fastest. Every year the dependency has widened, not narrowed.

This was a choice, and the same 2019 review said so:

Australia is an outlier in the global community in the way we think about liquid fuel security. When we consider countries of similar economies, most see fuel security as part of their strategic capability and take steps to manage fuel security with that in mind. Australia, by comparison, has chosen to apply minimal regulation or government intervention in pursuit of an efficient market that delivers fuel to Australians as cheaply as possible.

— Liquid Fuel Security Review, interim report, April 2019

Comparable countries treat fuel as strategic capability. Australia chose the cheapest delivered litre and let the market arrange the rest — while the volume at risk kept rising.

That outcome was not one decision but the sum of many, each rational on its own books and none weighed against the national whole — Britain made the same choices on the same logic and ended up just as exposed. The companion memo, The True Cost of "Cheap" Imported Fuel, traces exactly how it happened. What matters here is the result: the dependency widened, year after year, and it is still widening.

4. Why the refineries don't save us

Australia has two oil refineries left, at Geelong in Victoria and Lytton in Brisbane. They are often offered as proof that the country still makes its own fuel. They are not.

Table 2 — Australia's remaining refineries

| Refinery | Operator | Capacity (b/d) | Feedstock | Status |

|---|---|---|---|---|

| Geelong, VIC | Viva Energy | ~120,000 | imported crude | operating (supported to 2027+) |

| Lytton, QLD | Ampol | ~110,000 | imported crude | operating (supported to 2027+) |

| Total | ~230,000 | ~20% of demand | ||

| Closed 2014–21 | ~450,000 lost | Kurnell, Clyde, Bulwer Is., Altona, Kwinana |

Sources: Australian Petroleum Statistics; company reports; Liquid Fuel Security Review interim report 2019.

Both run on imported crude. Australia's own oil production is mostly light condensate the refineries cannot use and the country exports, buying back the heavier grades it needs — so even the fuel refined onshore depends on the same shipping lanes for its feedstock. Refining here does not break the dependency; it relocates one link of it. The two plants together turn out roughly 100,000 barrels a day of petrol and 80,000 of diesel — but national demand is skewed the other way, toward diesel, which is the fuel under the most stress in any disruption. The country lost around two-thirds of its refining capacity in a decade of closures, and what remains offers far less insulation than its existence suggests.

5. How far away our fuel is

The distance is not a detail. It is the exposure. Every litre Australia burns has to cross thousands of kilometres of ocean before it arrives, on a voyage that a single incident anywhere along the route can interrupt.

Table 3 — The journey to the bowser (indicative)

| Leg | Distance | Sailing time | Typical vessel |

|---|---|---|---|

| Persian Gulf → Asian refineries | ~6,600 nm | ~19–20 days each way | VLCC (~2,000,000 bbl crude) |

| Singapore → eastern Australia | ~4,000 nm | ~12–16 days | MR product tanker |

| South Korea → eastern Australia | ~5,000 nm | ~16–20 days | MR / LR product tanker |

| US Gulf/west coast → Australia | — | ~30–35 days | product tanker |

Sources: standard maritime route/voyage data; vessel-speed ~13–14 knots. Refined-product cargoes add port calls and transfers.

The fuel is not just imported; it is imported from a long way away, much of it refined in hubs that are themselves at the end of an even longer crude voyage from the Gulf. The crude reaches the Asian refinery after a three-week trip; the refined product then takes another two to three weeks to reach Australia. The pipeline that feeds an Australian service station is, in effect, five to six weeks long and runs past two of the most contested waterways on earth.

When a chokepoint closes, that pipeline does not just cost more — it lengthens. Diverting around the Cape of Good Hope adds one to two weeks to a voyage already measured in weeks, and in early 2026 vessels rerouted exactly that way. The supply line is at its longest at the moment it is under the most strain.

6. The tanker task — and why a small fleet can't carry it

To move ~850,000 barrels of refined product a day, Australia depends on a continuous conveyor of foreign tankers.

Table 4 — The import shipping task

| Measure | Figure |

|---|---|

| Refined product imported | ~850,000 b/d |

| Typical product (MR) tanker cargo | ~300,000 bbl (range 190,000–345,000) |

| Implied arrivals | ~3 cargoes a day, ~80–90 a month |

| Australian-flagged fuel tankers | 0 |

| Major Australian-flagged vessels (all types) | ~15 |

| Foreign-flagged ships carrying Australian trade (2019) | ~5,981 |

| Planned strategic fleet | ~12 ships |

Sources: Australian Petroleum Statistics; EIA tanker-size data; Australian General Shipping Register; MUA/Productivity Commission Vulnerable Supply Chains submissions, 2021; Strategic Fleet Taskforce.

There is not one Australian-flagged refined-product tanker on the register. A country that is the world's largest iron-ore exporter, second-largest coal exporter and fourth-largest user of ships owns almost none of the vessels its economy runs on. The fuel that keeps Australia moving arrives on roughly eighty to ninety foreign-flagged, foreign-crewed cargoes a month, dispatched by owners with no obligation to serve this country first — and, as the 2026 crisis showed, free to cancel or divert when the route turns dangerous.

In March 2026 the Energy Minister confirmed that six fuel cargoes bound for Australia in April had been turned back or deferred, amid concern that suppliers such as Malaysia and South Korea would hold fuel for their own needs. In a crisis the binding constraint is not only the price of a tanker but whether one can be secured at all, when every importing nation is bidding for the same foreign ships and Australia has no flagged fleet of its own to fall back on.

7. What it costs at the bowser

Diesel is the workhorse fuel of the Australian economy — the country draws more energy from diesel than from electricity. It moves the freight, runs the mines, drives the tractors and harvesters, and stands behind the hospital and the water plant when the power fails. When diesel gets dear or scarce, it does not stay in the transport column. It flows straight to the supermarket shelf, because nearly everything on that shelf arrived by diesel.

That is what 2026 made visible. The farmer who could not be sure of fuel for the harvest, the freight operator watching the margin vanish, the family in a remote town paying close to four dollars a litre — these were not abstractions. They were the predictable result of a fuel supply that runs through a chokepoint thousands of kilometres away, reaching the household budget within weeks of a shot fired in another hemisphere.

There is also a single point of failure most never see. About 99 per cent of Australia's heavy diesel trucks require AdBlue to run legally, and AdBlue is made from urea synthesised from natural gas. During the 2026 crisis Australia's urea stock was reported at around ten days of supply. Without AdBlue, the trucks that move the nation's food, medicine and fuel itself can stop — potentially before the diesel runs short.

8. The hidden cost — what the dependence charges us anyway

The crisis is the loud cost. There is a quieter one that runs even on a calm day, and it is rarely named.

Australia is a price-taker. With almost everything imported and no domestic buffer to release, the country pays whatever the world sets, and absorbs the world's volatility in full.

It pays that price twice over in a shock, through the currency. Fuel is priced in US dollars, and the Australian dollar tends to fall in exactly the global crises that push oil up — so a spike hits as a higher US price and a weaker dollar to meet it. The country gets struck on both sides of the same blow, and almost no one connects the two.

It pays the world's freight and insurance. Every litre carries tanker freight and war-risk insurance that land in the final price. In 2026 those costs went vertical — insurance for a single Gulf transit rising from a fraction of a per cent of a ship's value to several per cent, with freight surcharges stacked on top — and, as the analysts put it, it reaches the pump within weeks.

And it pays on ships it does not control, dispatched by owners and flag states that decide who gets served first in a crisis. None of these is the oil price. They are the toll for not supplying ourselves — and every one of them bites hardest in exactly the crisis the country can least afford.

There is also a bitter symmetry the companion memo costs out in full: the same shock that empties Australian pumps enriches the companies pumping Australian oil for export. The chokepoint that costs the motorist is a windfall for the producer — profit and pain on opposite sides of the same blow.

9. Two paths from here

Everything above describes the path Australia is on. From here the country has a choice between two, and it is worth setting them out plainly, side by side.

Path 1 — Stay on imports

This is the path of least resistance: keep importing around 90 per cent of the fuel, keep the thinnest reserves in the developed world, keep running on foreign ships through the same two chokepoints, and manage each crisis as it comes.

The government's current program is the best version of this path, and it is worth crediting honestly — but it is still this path. The 2026 Fuel Security and Resilience Package commits billions to build Australia's first permanent government reserve, around a billion litres of diesel and jet, aiming for fifty days of cover. The Strategic Fleet plan rebuilds a handful of Australian-flagged ships. Both are real. Neither makes a litre of fuel.

A bigger tank is not a supply: it holds more of a fuel the country still does not make, fifty days is still short of ninety, and a stockpile drains. The fleet is a dozen ships against an import task of eighty to ninety tanker cargoes a month — years to build, still carrying imported fuel through the same chokepoints. And in the 2026 crisis itself the response was the same shape: the government released up to 762 million litres (762 ML) from reserves, lowered fuel-quality standards to add roughly 100 million litres (100 ML) a month, convened a taskforce, and modelled rationing. Every measure moved or stretched existing fuel. None made any.

Table 5 — The reserve, against the obligation (days of cover)

| Fuel / measure | Days |

|---|---|

| Petrol | ~39 |

| Diesel | ~29 |

| Jet fuel | ~30 |

| Path 1 target (the $14.8bn tank) | 50 |

| IEA obligation | 90 |

| IEA member average | ~140+ |

| 2026 rationing-model trigger (diesel) | ~10 |

Sources: IEA oil-stock data; DCCEEW fuel-security reporting; 2026 contemporary reporting. Reserve measures differ in definition; figures are indicative.

That is the ceiling of Path 1. At its very best it buys time and cushions the shock. It cannot end the exposure, because the exposure is the path. Staying on imports is a permanent subscription to the vulnerability — and, as the companion memo The True Cost of "Cheap" Imported Fuel sets out, a standing bill of about $59 billion a year (2023, and rising) that leaves the country and builds nothing here.

Part of that cost is easy to miss because it looks like help. In the 2026 crisis the government also halved the fuel excise for three months — about $2.9 billion in revenue it chose to forgo so the pump price would not climb further. That is the move of a country with no other lever: a price-taker imports the world price and its inflation with it, where a producer that owns its supply can steady the domestic price and absorb the shock instead of passing it on. Part 1 counts both the forgone revenue and that pricing sovereignty in full.

Path 2 — Make it here, and export the surplus

The other path reverses the arrangement. Cut the demand that can be cut, make the fuel that is left at home, and turn what the country can produce beyond its own needs into exports. This is more than self-sufficiency: it is the move from importing finished fuel to manufacturing it — and, carried far enough, exporting it. The next section sets out how that is built. The choice between the two paths is stark:

| Path 1 — Stay on imports | Path 2 — Make it here, export the surplus | |

|---|---|---|

| Price at the bowser | World price, full volatility, currency-multiplied | Domestic, stable, AUD-priced |

| Supply security | ~30-day buffer; chokepoint + tanker exposure | Made at home; immune to chokepoints |

| Where the money goes | ~$59bn/yr offshore (2023, rising), permanently | Stays onshore, recirculates |

| Trade position | Net importer of finished fuel, forever | Net exporter of finished and clean fuel |

| Jobs & industry | Offshore | Refining, biofuels, hydrogen, rail, regional |

| In a crisis | Buy, borrow, ration, wait | Already supplied |

| What it builds | Nothing — rents protection | A permanent, exportable industry |

| Cost | Cheaper per litre today; a bill that never stops | Dearer upfront; an investment that pays back |

Path 1 is cheaper today and more expensive every year after, forever. Path 2 costs more to start and then keeps paying — in money that stays home, in crises that don't happen, and in an industry that exists, and earns, at the end of it.

10. Becoming a net exporter

Self-sufficiency is the floor, not the ceiling. Australia is already one of the world's great energy exporters — of raw crude, gas and coal. What it is not is an exporter of finished fuel: on transport fuel it is among the most import-dependent nations in the developed world. It ships raw energy out and buys refined fuel back, handing the value-adding middle to others and keeping the strategic risk for itself.

The prize is to flip that. The same build that ends the dependency, carried far enough, makes Australia a net exporter of finished and clean fuels to a region that will need them. Each lever below first replaces an imported litre; together, and at scale, they turn a standing import bill into an export industry.

Electrify the bulk of demand away. Every tonne-kilometre moved off imported diesel is a barrel the country never ships in. Freight shifts to electrified rail along the national corridor; passenger vehicles go electric; mining and agricultural fleets electrify; high-speed rail removes much of the domestic aviation task. The single largest prize is ordinary: an all-electric passenger fleet alone would replace roughly a third of Australia's imported oil with domestic electricity. Demand removed is demand that never has to be imported or made — and it frees domestic energy for higher-value use, including export.

One policy pulls hard against this. The Fuel Tax Credit scheme refunds the excise on off-road and heavy-vehicle diesel — about $10 billion a year and rising — which keeps imported diesel artificially cheap and, by one major miner’s own analysis, roughly halves the return on switching a fleet to electric. It is a standing public cost of the import model (Part 1 counts it in the ledger), and redirecting it — from rebating imported diesel to backing electrification and domestic fuel — is among the faster levers available.

Make the fuel that's left — and then some. What cannot be electrified — long-haul aviation, shipping, heavy industry — is made from what the country grows. Australia already grows fuel: after the 2025–26 harvest, around 5.84 million tonnes of canola sat in Australian silos — roughly 2.2 billion litres of biodiesel equivalent, about 34 to 37 days of national diesel, needing no tanker, no Gulf, and no foreign government's permission. A standing rule reserving half of each year's crop for domestic processing would yield 1.1 to 1.3 billion litres a year — 18 to 22 days of diesel from domestic feedstock, every year. Beyond biodiesel sit renewable diesel and sustainable aviation fuel (SAF), made from the same and additional feedstocks — products the world is short of and willing to pay a premium for. The feedstock base is here; the processing is the gap to close.

Find, produce and refine our own oil. The claim that Australia has no oil is a claim about price, not geology — and it is undercut by the fact that the country stopped looking. Dorado, off the Pilbara coast, was the largest oil discovery in Western Australia this century, found in 2018 in the lightly drilled Bedout Sub-basin — a basin with around seventeen exploration wells against more than fifteen hundred in the basin next door — by a well that was chasing gas. It is light, low-emission crude, headed for first oil around 2026. Dorado is not alone: the same sub-basin holds further discoveries and leads, and the Great Australian Bight remains essentially untested. A serious, sovereign exploration effort across the frontier basins is overdue and should begin now. And the oil it finds need not leave the country to be refined: modular refineries — skid-mounted units built in under a year, at a fraction of the cost of a legacy plant and matched to exactly the light condensate Australia produces — can process it onshore. Refining capacity, once built, can take more than domestic crude: it turns feedstock into finished product for sale, the value-adding step Australia abandoned when its refineries closed.

Turn gas and renewables into liquid fuel. Australia sits on some of the world's largest gas reserves and its best solar and wind, and both can be turned into transport fuel. Gas-to-liquids technology — proven at commercial scale at Shell's Pearl plant in Qatar — converts natural gas into clean diesel and jet fuel. Green hydrogen, made by splitting water with surplus renewable power, becomes green ammonia, e-methanol and synthetic e-fuels: zero-carbon fuels for shipping, aviation and export. These cost more per litre today and need scale and time; their case is not present cost but strategic position. Australia has the gas, the sun, the wind and the land to make them in volumes far beyond its own use — which is exactly what an export industry requires. (Coal-to-liquids is technically proven too, but its emissions rule it out as anything but a last resort; the clean routes are the ones worth building.)

Keep the reserve in the ground. A built stockpile is the weakest form of reserve, and the companion memo sets out why in full. Keep a real onshore stockpile as the bridge — but the coal, gas, standing crop and undeveloped basins are a reserve that costs nothing to store, cannot be sunk or embargoed, and never empties.

Then export the surplus. Put the levers together and the arithmetic moves one way. Demand falls as the country electrifies; domestic output of biofuel, refined product and synthetic fuel rises; the gap filled by imports today closes, then reverses. At that point Australia is no longer buying finished fuel from the Asia-Pacific — it is selling finished and clean fuel into it: refined product, renewable diesel, sustainable aviation fuel, green ammonia and e-methanol, to a region of energy-hungry economies sitting on the same chokepoints Australia is escaping. The country that today exports raw energy and imports finished fuel would instead make the finished fuel and sell it. That is the link to the wider strategic picture in the companion memo The Prize: A Unified AsiaPac, and the industrial heart of the New Deal build — not an expense to be minimised, but a permanent industry to be stood up.

11. The payoff

Done this way, fuel sovereignty is not a cost the country bears for security. It is cost-of-living relief, national security, and an export industry bought with the same money.

The household with an electric car is unhooked from the bowser and the Gulf at once. The freight that moves by electrified rail does not price a war-risk premium into the groceries. The dollars that today leave the country to buy refined fuel stay here, building the rail, the generation and the plants that make the fuel — and then earn again, selling the surplus abroad. The same spend the government is committing to a fifty-day tank, redirected, builds the thing that retires the dependency instead of cushioning it — and a country that can fuel and move itself can defend itself, which the companion defence memos take up in full.

12. Conclusion

Australia's transport-fuel problem is not a shortage of energy. It is a country that produces energy in abundance and has chosen, year after year, to export it raw and buy the finished fuel back — holding the thinnest reserve in the developed world, on ships it does not own, through chokepoints it does not control, while the bill and the volume both climb.

None of that is fixed by a bigger tank or a handful of ships. Those buy time. What ends the exposure is reducing the demand that can be reduced and making the fuel that remains — and the same build, carried to its conclusion, does more than close the gap. It turns the largest standing import bill in the economy into an export industry, and a strategic weakness into a regional strength.

The companion memo, The True Cost of "Cheap" Imported Fuel, shows this is also the cheaper path once the whole ledger is counted. This memo shows it is the achievable one. Australia has the crude, the gas, the sun, the wind, the land and the grain to fuel itself several times over. The only question its fuel supply has ever really posed is whether it will use that energy to supply itself first, and supply the region second. The answer, so far, has been no. It does not have to stay that way.

References

- Production (~400,000 b/d petroleum liquids, 2024; >94% of domestically produced oil exported) — EIA Australia Country Analysis 2025; Geoscience Australia, Australia's Energy Commodity Resources 2025; Worldometer/EIA.

- Consumption (~1,150,000 b/d) and import share (~90% of refined fuel) — Australian Petroleum Statistics (DCCEEW); IEA.

- Refineries (Geelong ~120,000 b/d; Lytton ~110,000 b/d; ~20% of demand; petrol/diesel split) — Australian Petroleum Statistics; company reports.

- Reserves (~30 days key fuels; IEA 90-day obligation unmet since 2012; member average >140 days) — IEA oil-stock data; DCCEEW.

- Sailing distances/times and tanker capacities (MR ~190,000–345,000 bbl; Gulf–Asia ~19–20 days each way) — standard maritime route data; EIA tanker-size classification.

- Shipping task and fleet (no Australian-flagged fuel tanker; ~15 major Australian-flagged vessels; ~5,981 foreign-flagged ships, 2019) — Australian General Shipping Register; MUA and Productivity Commission Vulnerable Supply Chains submissions, 2021.

- Currency, freight and war-risk insurance — maritime insurance market reporting, 2026.

- Fuel Security and Resilience Package (A$14.8B; ~1bn-litre reserve; 50-day target) — government announcement, May 2026; Strategic Fleet Taskforce.

-

Electrification lever (all-EV passenger fleet ≈ one-third of imported oil replaced) — IEA; IEEFA; The Australia Institute (data attributed to underlying government sources).

-

Canola stocks and biodiesel potential (~5.84 Mt in storage; ~2.2 billion litres biodiesel equiv.; 50% standing hold ≈ 1.1–1.3 bn L/yr) — MMP fuel-crisis letter series (Letter 7, 31 March 2026), drawing on ABARES crop data.

- AdBlue/urea exposure (~99% of heavy trucks; ~10 days urea stock) — MMP fuel-crisis letter series (Letter 3, 6 March 2026); ministerial statements, March 2026.

- 2026 government response (762 ML reserve release; fuel-standard relaxation ~100 ML/month; rationing modelled; no emergency declared; six April cargoes turned back) — contemporary reporting (SBS, The Nightly, IBTimes), March 2026; Energy Minister statements.

- MMP fuel-crisis letter series, 7 letters, 3–31 March 2026 — public record at moralmajority.com.au/documents.html.

- Importance of liquid fuel + Australia as fuel-security outlier (quoted) — Liquid Fuel Security Review, interim report, April 2019 (Department of the Environment and Energy); final report never released.

- Diesel import volumes 2012–2023 (11.24 → 29.8 thousand megalitres; ~91% imported by 2025) — Australian Petroleum Statistics (DCCEEW), compiled by the author.

- Dorado / Bedout Sub-basin (largest WA oil discovery this century, 2018; ~17 exploration wells vs >1,500 in the neighbouring Carnarvon Basin; light low-CO2 crude; first oil ~2026) — Wood Mackenzie; 3D Energi; Carnarvon Energy / Petroleum Economist.

- Modular / mini refineries (skid-mounted, built in under a year, lower installed cost than a legacy plant, topping/splitter configuration suited to light condensate) — industry sources (Honeywell UOP; Howe Baker).

- Oil-producer windfall during the 2026 shock (six largest majors projected ~US$94bn for the year) — Oxfam International, 2026; Fortune; company results.

- Gas-to-liquids at commercial scale (natural gas to clean diesel and jet) — Shell Pearl GTL, Qatar; GTL technical literature.

- Green hydrogen, ammonia and synthetic e-fuels from surplus renewables; Australia's renewable-energy and clean-fuel export potential — CSIRO; ARENA; industry assessments.

- Sustainable aviation fuel and renewable diesel — feedstock base and demand outlook — IATA; renewable-fuels industry sources.